The “cool kid” of the manufacturing world has finally grown up. A decade ago, Additive Manufacturing (AM) was the go-to for hobbyists and rapid prototyping. Today, in 2026, it is the backbone of the American industrial renaissance. From rocket engines to patient-specific spinal implants, 3D printing has moved off the lab bench and onto the high-volume factory floor.

If you are a manufacturer in this space, the landscape has never looked more promising, or more complex. Here is the definitive breakdown of where the industry stands and why the “Exit Window” is currently wide open.

A Decade of Velocity: 2016–2036

In 2016, the U.S. AM market was a modest $2.1 billion sector. Fast forward to today, and we are looking at an $8.2 billion powerhouse. But the real story is what happens next. By 2036, the U.S. market is projected to skyrocket to nearly $48 billion, fueled by a 21.6% CAGR. We are no longer just “printing parts”; we are integrating AI-driven design and real-time sensor monitoring to create components that were physically impossible to manufacture just five years ago.

The Material Shift: Metals vs. Polymers

While polymers still hold the majority of the volume (around 52%), Metal AM is the high-value sprinter. With a projected growth rate of 24.7%, titanium and nickel alloys are dominating the Aerospace and Defense sectors. Meanwhile, Composites are carving out a niche in lightweight UAV frames and high-strength tooling.

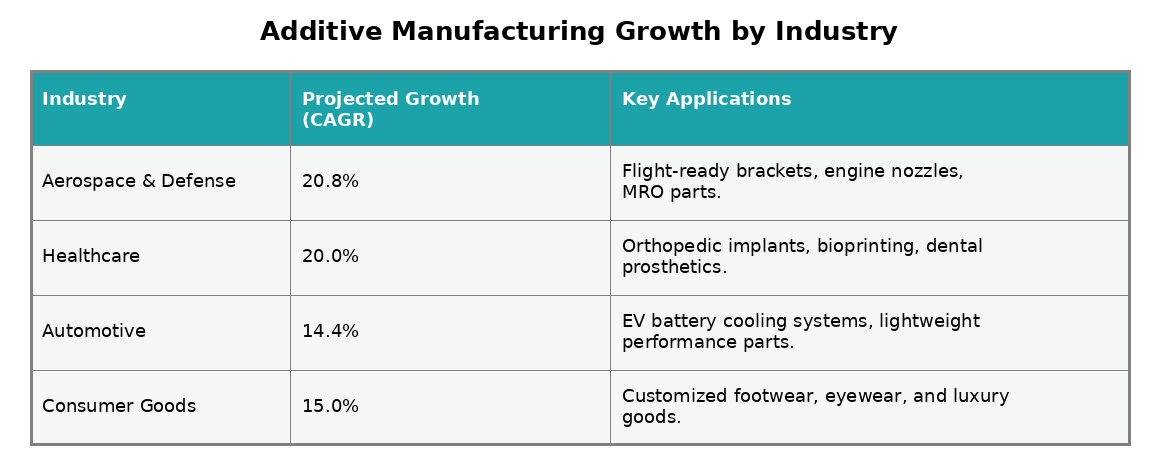

Market Performance by Sector

The “Digital Thread,” the seamless connection from design to finished part, is being pulled through every major industry.

The M&A Landscape: Multiples and Momentum

The last 24 months have seen a “K-shaped” recovery in M&A. While general manufacturing has faced headwinds, Additive Manufacturing remains a “hot” sector for both strategic buyers and Private Equity (PE) firms.

Transaction Multiples at a Glance

- Strategic Buyers: Currently paying 11x to 15x EBITDA. They are hungry for intellectual property and specialized material expertise.

- Private Equity: Hovering around 9x EBITDA. PE firms are looking for “platform” companies they can use to roll up smaller service bureaus.

- Lower Middle Market (LMM): For companies with $1M–$5M in EBITDA, we are seeing multiples between 6.5x and 8.5x, depending on the “moat” the business has built.

Valuation Driver Tip: In 2026, a machine is just a machine. Buyers are paying for certifications (AS9100D, ISO 13485) and long-term production contracts. If you are still 90% prototyping, your multiple will suffer.

5 Reasons to Consider Selling in 2026

If you’ve been building your AM business for years, the current climate offers a rare alignment of stars. Here is why savvy owners are looking for the exit:

- The “Scale Premium”: Strategic acquirers are currently paying a premium to achieve domestic scale to compete with global conglomerates.

- CapEx Burnout: The next phase of AM requires massive investment in AI-integrated hardware and robotic post-processing. Selling allows you to let a larger partner foot the bill for the next tech cycle.

- The Talent War: Finding AM engineers is harder than finding a needle in a haystack. Joining a larger organization solves the recruiting headache.

- Reshoring Incentives: Federal policies are currently favoring U.S.-based advanced manufacturing. This has artificially inflated the value of “Made in USA” shops—a window that may not stay open forever.

- De-risking the Future: With EBITDA multiples at historical highs for the sector, many owners are choosing to “take some chips off the table” before potential shifts in interest rates or trade tariffs in 2027.

The Bottom Line

Additive Manufacturing has transitioned from a curiosity to a necessity. For the Lower Middle Market owner, your business is no longer just a “3D printing shop,” it is a critical link in the American supply chain. Whether you plan to scale or sell, the data suggests that the next 24 months will be the most consequential in the industry’s history.