The ammunition sector is currently experiencing unprecedented procurement velocity driven by the convergence of high-intensity global conflicts and a fundamental re-industrialization of the American defense base. For owners of lower-middle-market (LMM) defense firms, those typically valued between $10M and $150M, the current climate presents a rare window of “perfect market timing” for exit or recapitalization.

Last week’s White House summit with major defense primes (Lockheed Martin, RTX, Northrop Grumman) signaled more than just a production boost; it signaled a multi-year commitment to domestic supply chain resilience that trickles directly down to the component manufacturers.

Market Snapshot: Size & Growth (2026–2035)

The ammunition market has shifted from a stable, low-growth commodity sector to a high-velocity strategic industry.

- Current Market Value (2026): Estimated at $32.4B to $34.8B globally, with North America commanding approximately 41% of the total share.

- Projected Growth: Analysts project the market will reach between $53.6B and $66.1B by 2035.•

- Compound Annual Growth Rate (CAGR): Estimates vary by sub-segment, but the overall market is expected to grow at a 7.5% to 13.7% CAGR over the next decade.

- Segment Outperformers: Large-caliber munitions and precision-guided components are expected to lead with growth rates as high as 16.6%.

Why the “Lower Middle Market” is the New Battleground

While the “Primes” (the Tier 1 contractors) capture the headlines, they are increasingly dependent on Tier 2 and Tier 3 suppliers to meet the White House’s mandate to quadruple production of “Exquisite Class” weaponry.

1. The Multi-Year Backlog

The Pentagon has secured multi-year procurement authorities for at least eight major missile and munition types. For a business owner, this converts “speculative interest” into “guaranteed revenue,” significantly increasing the EBITDA multiples during a business valuation.

2. The “Re-Industrialization” Premium

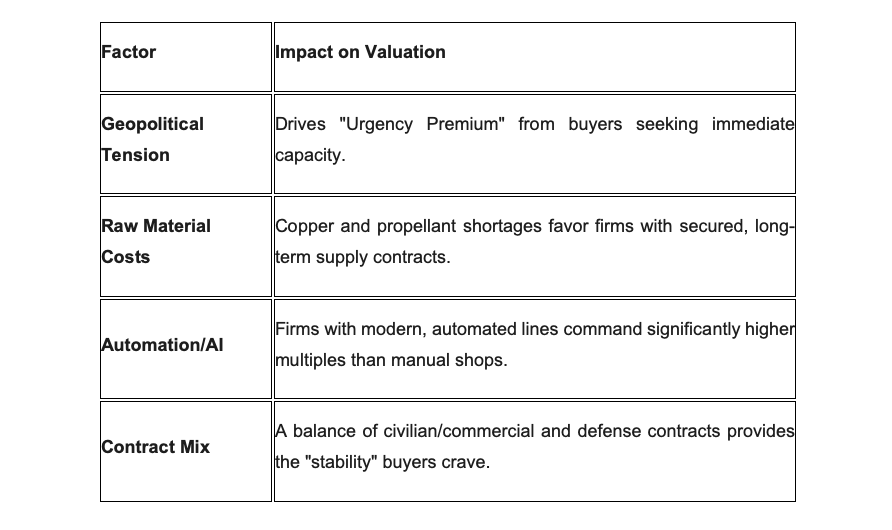

The Trump administration’s focus on domestic manufacturing means that “Made in America” is no longer a preference, it’s a requirement. LMM firms specializing in CNC machining, solid rocket motor components, or specialized primers are seeing a “scarcity premium” as larger firms look to acquire capacity rather than build it from scratch.

3. M&A Dynamics: The Exit Window

Strategic buyers and Private Equity (PE) firms are aggressively pursuing LMM acquisitions to:

- Secure the Supply Chain: Ensuring they aren’t throttled by a single-source component supplier.

- Capture Innovation: Acquiring “Expeditionary Manufacturing” capabilities (e.g., 3D printing, AI-driven quality control).

- Deploy Dry Powder: PE firms have significant unspent capital and are looking for stable, defense-backed cash flows to hedge against broader economic volatility.

Strategic Considerations for Retiring Owners

If you are considering an exit in the next 18–36 months, the current surge provides a unique opportunity to capitalize on peak valuation.

The “Retirement” Pivot

For owners who have weathered the supply chain storms of the early 2020s, the current $50B+ supplemental funding requests and the “Golden Dome” missile defense initiatives offer a graceful exit. Buyers are currently looking for durability over potential; a shop with a clean balance sheet and a three-year order backlog is the most attractive asset in the current M&A landscape.