Market Size, Growth, EBITDA Multiples, and 5 Reasons Owners May Consider Selling Now

The defense drone manufacturing market has moved from a promising niche into one of the most closely watched segments of the aerospace and defense industry. Demand is being driven by battlefield urgency, procurement reform, and a growing push for secure domestic manufacturing capacity. For owners of lower middle market drone manufacturers, that combination is creating a meaningful question: is this the right time to consider a sale?

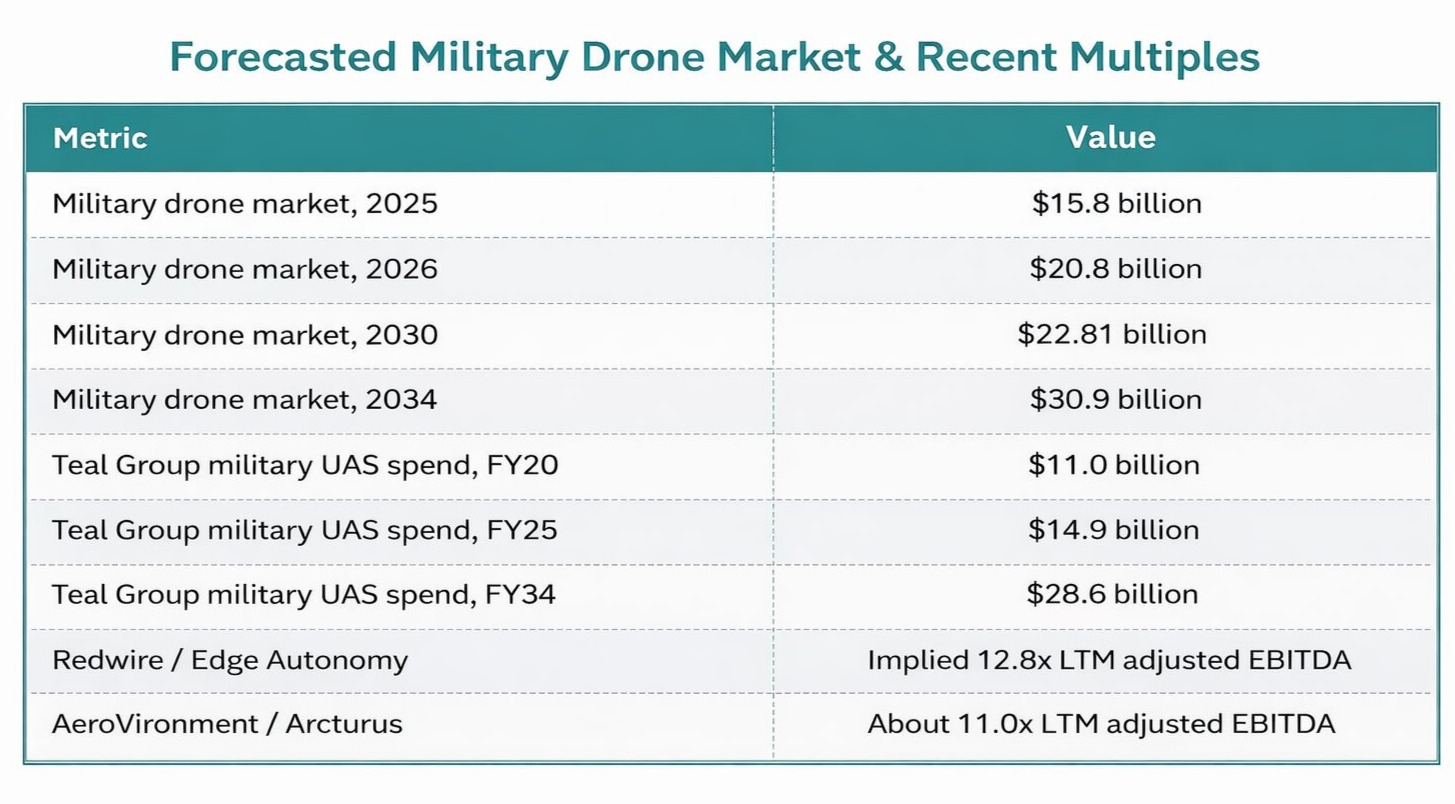

The numbers suggest the sector is expanding on multiple fronts. MarketsandMarkets estimates the global military drone market at $15.8 billion in 2025 and projects it will reach $22.81 billion by 2030, a 7.6% compound annual growth rate. Fortune Business Insights estimates the market at $20.8 billion in 2026 and projects it will reach $30.9 billion by 2034, implying a 6.8% CAGR from 2026 to 2034. On a spending basis, Teal Group reports that worldwide military UAS spending on unclassified research, development, testing, evaluation, and procurement rose from about $11 billion in FY20 to about $14.9 billion in FY25 and is projected to reach about $28.6 billion by FY34, or about 7.5% annual growth over that period.

In plain English, the market is not just getting larger. It is becoming more important to national defense planning, more relevant to strategic acquirers, and more demanding for independent manufacturers that need capital, compliance infrastructure, and production scale.

- Demand is rising, but scaling is getting more expensive.

The market outlook is attractive, but growth now comes with higher expectations. Defense customers increasingly want low cost, attritable, rapidly fielded systems, and governments are sending clear signals that production volume matters. The Pentagon’s July 2025 drone-dominance memo called drones the biggest battlefield innovation in a generation, and the War Department later said it wanted industry support for more than 300,000 drones. For an independent manufacturer, that can mean heavier working-capital needs, more investment in supply chain resilience, and greater pressure on production throughput. Selling to a larger strategic buyer can provide the capital and infrastructure needed for the next stage of growth. - Strategic buyers are looking for domestic manufacturing capacity now.

The policy backdrop has become more favorable for American drone manufacturing. The Pentagon’s 2025 memo explicitly emphasized strengthening the domestic industrial base and buying American. That gives added value to companies with U.S.-based production, secure sourcing, compliant components, and a manufacturing footprint that can support defense procurement. In many cases, those capabilities are worth more to a strategic buyer today than they were only a few years ago. - Valuations can benefit from scarcity and urgency.

There are still relatively few lower middle market drone manufacturers with real defense-customer traction, scalable production capability, and credible program access. When larger buyers need to deepen their unmanned systems position quickly, acquisition is often faster and less risky than building internally. Recent disclosed transactions support that logic: AeroVironment’s acquisition of Arcturus was disclosed at about 11.0x LTM adjusted EBITDA, and Redwire’s acquisition of Edge Autonomy implied about 12.8x LTM adjusted EBITDA. - The market is shifting from product innovation risk to execution risk.

A few years ago, many drone businesses were valued largely on technology potential. Today, buyers are asking a harder question: can this company deliver quality products at scale, on time, and within defense procurement constraints? Owners who have already built viable products, established manufacturing discipline, and developed customer credibility may be in a strong position to sell before parts of the market become more crowded or more price competitive. - The strategic window is open while defense priorities remain highly visible.

Military drone demand has been reinforced by recent battlefield lessons, procurement reform, and defense budget priorities in the United States and allied markets. When a sector is not only growing, but also viewed as strategically urgent, buyer attention tends to increase. That can create a favorable environment for a well-positioned manufacturer to explore a transaction while the segment is still commanding outsized strategic interest.

What Drives Valuation in the Lower Middle Market

For a lower middle market defense drone manufacturer, valuation usually comes down to more than just current EBITDA. Buyers pay up for businesses that can reduce execution risk and accelerate access to the market. The most important drivers tend to include defense-customer traction, repeat orders, funded programs, production scalability, domestic sourcing, secure supply chains, autonomy or payload differentiation, and strong quality systems.

The underlying theme is simple. A company that can move from prototype to dependable output is worth more than a company that still needs major industrialization work. Likewise, a manufacturer that already fits current procurement priorities, including domestic manufacturing and resilient sourcing, is often more attractive than one that would require a buyer to rebuild the platform after closing.

![]()

Bottom Line

The defense drone manufacturing market is expanding, but it is also becoming more demanding. Owners are operating in a sector where the addressable market is rising, buyer interest is increasing, and strategic acquirers may be willing to pay meaningful multiples for the right capabilities. At the same time, scaling independently is becoming more capital intensive and more operationally complex.

For a founder who has already built a differentiated business, this may be one of the more attractive windows in recent years to evaluate strategic options.

Thinking about an exit?

If you own a defense-related drone manufacturing business and want to understand how buyers may value your company in today’s market, a confidential market review can help clarify timing, likely acquirers, and the steps that drive premium value.